29 November 2024

Passengers wait for a train at Cape Town station. The City proposes to take over management of the network from PRASA, with trains eventually running as often as every three minutes by 2052. Photo: Steve Kretzmann

Passenger rail, which should be the backbone of Cape Town’s public transport system, has been in decline for a decade under PRASA’s management, losing 92% of passenger trips since the 2012/13 financial year.

Figures provided by PRASA state there were 172-million passenger trips on the Cape Town’s rail network in 2012/13, and just 13-million during 2023/24.

An investigation into the feasibility of the City running the local rail network instead of PRASA, says the City could not only return the rail service to 2012 levels, but could build new lines and provide about 54,000 new housing units on vacant or underutilised land around the city’s 92 train stations.

Proper management of the 48 hectares of leasable land currently in PRASA’s hands could see the train stations – many of them dilapidated – become hubs of activity with offices, residential units and businesses.

Larger stations could also house government services.

However, this would entail close to R100-billion in development costs over the next 30 years.

The new report, which has been in the making since July 2022, is to be set before the city council for approval on 5 December.

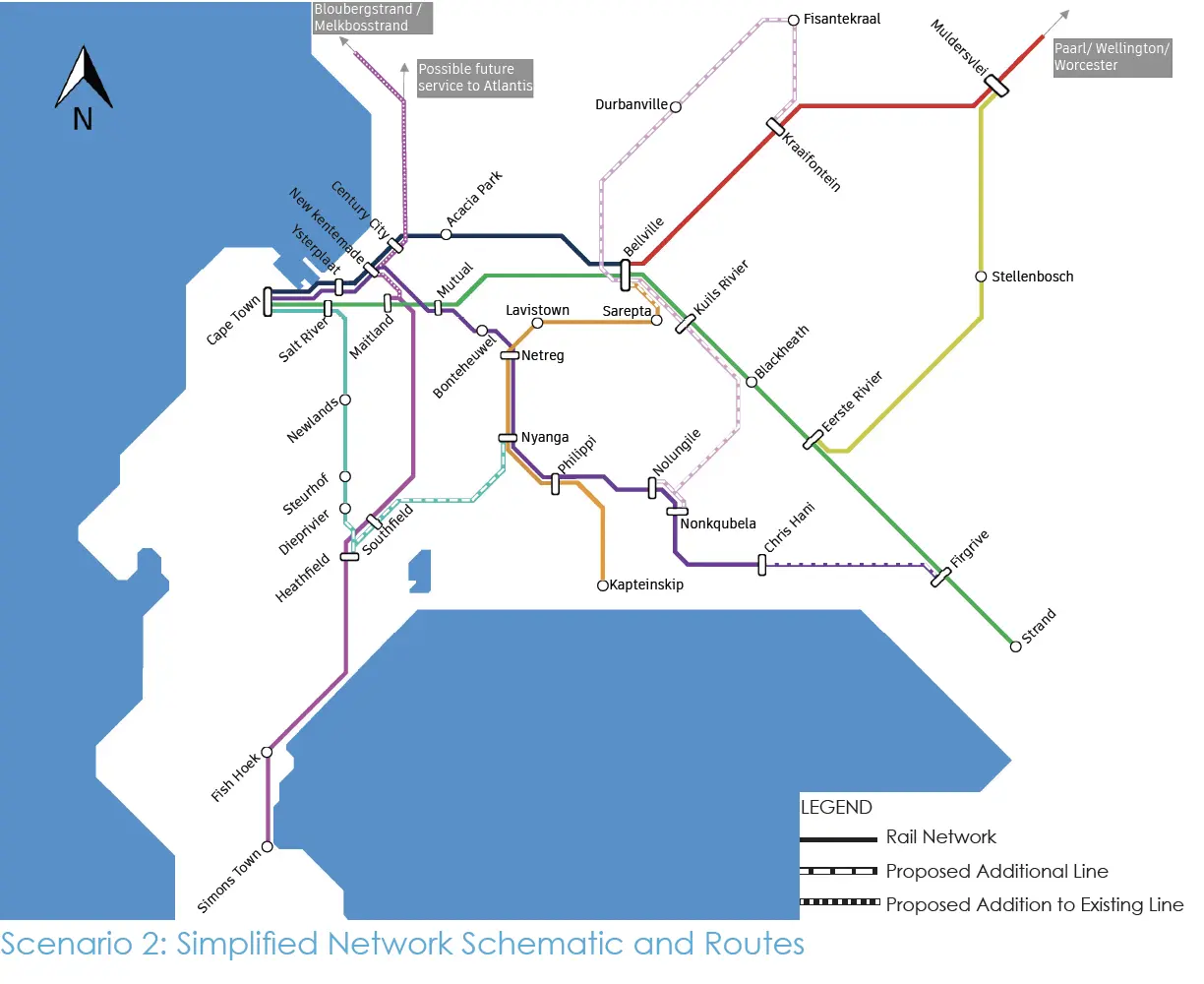

It looks at three scenarios, including the network remaining as is, but favours a reconfigured network listed as Scenario 2, with a number of new lines including east-west lines across the southeast metro and a new line going north to Bloubergstrand.

A Blue Downs Line, which has long been planned, would run between Steurhof and Philippi stations to join the existing Central Line, and then extend from Nolungile station to Kuils River station, allowing commuters to travel between Bellville and Diep River without going via Cape Town station.

A new line from Maitland station to Blouberg, servicing suburbs such as Parklands and Table View, and a new line linking Bellville to Kraaifontein via Durbanville and Fisantekraal, are also proposed.

An alternative direct route from Simon’s Town to Cape Town would run via the Central Line rather than the Southern Line, which is presently the direct line. The Central Line currently terminates at Heathfield. People travelling between Simon’s Town and stations between Heathfield and Cape Town – such as Newlands or Observatory – would have to change trains at Heathfield. This is because the Southern Line has relatively low demand compared to other lines. This preferred scenario, listed as Senario 2, involves certain lines being run by a private operator.

The cost calculations are fairly opaque, but the report, which is a high-level executive summary, states that there is detailed analysis in accompanying technical reports to which GroundUp has not yet obtained access.

However, the study notes that even in Scenario 0, the cumulative capital expenditure involved in getting the rail network back to transporting approximately 190-million passengers a year by 2032 will be R6-billion.

This is largely made up of procuring new rolling stock to increase the number of trips from 707 to 981 per weekday. For Scenario 2, the cumulative capital expenditure for rolling stock and infrastructure is calculated at about R21-billion by 2042.

The cost of operating the service increases as more train sets are included on the lines, but tops out by 2052 at about R3.3-billion per year for Scenario 0, and about R3.6-billion annually for Scenario 2. This is more than the projected fare revenue for 2052, which is calculated at R1.8-billion per year for Scenario 0, and R2.9-billion for Scenario 2. This does entail fare increases. (Commuter rail is subsidised in many cities across the world.)

The study notes that rail customers are very sensitive to fare increases, and that with every 1% increase in the fare, there is a 0.37% loss in customers. The balance struck is an 80% fare increase, which would come with a 30% loss in customers. Currently, one-way fares are R18 return during peak hours. An 80% increase would peg that at R32.40.

Perversely, there is an incentive to have fewer customers, as it reduces capital and operational expenditure, but it is noted that the point of the rail service is to provide “an affordable and low-cost transport alternative that is available to all communities”.

Although income from fares will not cover operational expenditure in any of the scenarios, the study suggests income from the use of state-owned land at and around the train stations “represents a viable path towards the sustainable implementation of a modernised passenger rail system for Cape Town”.

This needs to be “underpinned by strong town planning and infrastructure development”, which could “transform the city’s transportation network and urban landscape”.

Simply maximising revenue potential from the existing stations could increase income from “non-fare revenue” from the current R46-million a year to R777-million a year.

However, the City looked at developing 110 vacant or underutilised parcels of land situated around 25 stations, and projects an annual rental income of R6.2-billion from these. This includes 54,000 new residential units of different sizes that could be built, as well as shops, offices, and industrial properties at stations such as Ndabeni. This would not only provide an income stream but also stimulate economic activity and urban densification around these stations.

Generating this revenue does, however, entail development costs of R88.5-billion for the 25 stations analysed. These figures indicate it would take more than 14 years, excluding maintenance, to recoup this capital expenditure before it could start subsidising the rail operating costs.

While there are three overall scenarios for the recovery and development of the rail network, there are five potential structures listed for the institutional arrangements between the City of Cape Town, PRASA, and the Western Cape Government.

These range from PRASA retaining ownership of the network as is, ownership being transferred to the City, ownership being transferred to the provincial government, a hybrid option in which the City has the authority to grant concessions to private operators, and a fifth option in which the City has concessional authority over the entire rail network. Some of these have sub-options.

The options are scored according to a matrix that includes risks, cost benefit, institutional mandates, and existing planning policy.

Overall, the report favours what is listed as Sub-Option 2.1 in which the City owns, operates and maintains the network, and Sub-Option 2.2 in which the City owns the assets but provides concessions to a private operator.

The option with the least risk while still meeting the objectives of a reliable rail service, according to the report, would be a private operator running the entire network and managing the assets.

All of these ownership arrangements would involve expansion of the current network with an increased number of train sets seeing trains running as often as every three minutes on some lines during peak periods.

The national Department of Transport was approached for comment on the possibility of the City running the local rail network, but no response was received before publication.

Should the report be approved by council, a business plan for rail management will be developed.